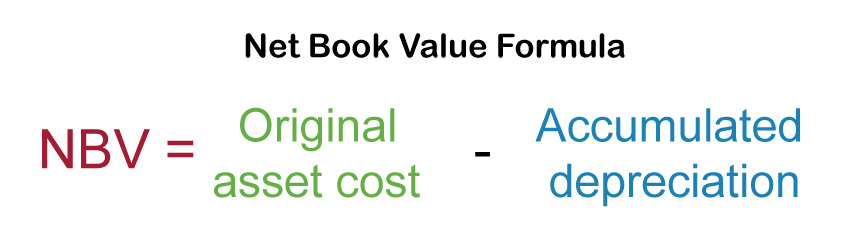

Why is Accumulated Depreciation a Credit Balance?Understanding Accumulated DepreciationThe cumulative depreciation of an asset that has been recorded since the time it was put in use is known as accumulated depreciation. Long-term investments include fixed assets such as real estate, machinery, and equipment. Depreciation consumes a portion of the asset's cost in the year of purchase and every year after that for the rest of the asset's useful life. Investors and analysts can determine how much of the total price of a fixed investment has been depreciated by looking at accumulated depreciation.  The value of any fixed asset depreciates over time, and hence the cost incurred is not the same as the year it was purchased. Depreciation enables a business to stretch out the expense of investment throughout the asset's useful life to generate revenue from the purchase. Depreciation prevents a significant cost from being recorded in the year an asset is purchased. The whole amount of depreciation expense that has been incurred thus far for the asset is kept in an account called accumulated depreciation. In other words, it represents a running sum of all depreciation costs that have been tallied over time. Why is Accumulated Depreciation a Credit Balance?Accumulated depreciation is a contra-asset account that is used to offset the asset account to which it pertains, making it a credit balance. As a business invests in long-term assets like real estate, machinery, and equipment, it depreciates those costs over time. It is essential for businesses to align investment costs with the income they produce. Each period, depreciation is charged to the income statement, which lowers the company's net income. The accumulated amount of depreciation is recorded in the balance sheet as an account called "Accumulated Depreciation". This account has a credit balance because it is a contra-asset account. An account that is used to lower the value of an asset account is known as a contra-asset account. In this instance, accumulated depreciation lowers the long-term asset's book value. The reason why Accumulated Depreciation has a credit balance is that it is the opposite of the normal balance of an asset account. An asset account typically has a debit balance because it represents something the company owns and has value. On the other hand, accumulated depreciation is a negative asset account. It refers to how much of an asset's worth is used up over time. For example, if a company purchased a piece of equipment for $10,000 and depreciated it by $1,000 yearly for three years, the accumulated depreciation would be $3,000 ($1,000 x 3). As a result, the equipment's book value would be $7,000 ($10,000 - $3,000). A credit balance arises from the $3,000 in accumulated depreciation because it lowers the equipment's book value. Accumulated depreciation is important for financial reporting and analysis because it helps to accurately reflect the value of long-term assets on the balance sheet. It also helps to spread the cost of the purchase over its useful life, which can reduce the tax burden on the company. Finally, it provides a clear picture of the asset's value at any given time, which can be helpful for decision-making. Contrary, since accumulated depreciation is a contra-asset account that lowers the book value of a long-term asset on the balance sheet, it results in a credit balance. It is important for financial reporting and analysis because it accurately reflects the importance of long-term investments and helps to spread the asset's cost over its useful life. What are the benefits of Accumulated Depreciation?Accumulated depreciation provides several benefits to a company. First, it helps to accurately reflect the book value of long-term assets on the balance sheet. Second, it helps to spread the asset's cost over its useful life, which can help reduce the tax burden on the company. Finally, it helps to provide a clear picture of the asset's value at any given time, which can be helpful for financial analysis and decision-making. What is the Net Carrying Amount?Net carrying amount, also known as net book value, is the amount at which a company's asset is carried on the balance sheet after accounting for accumulated depreciation and impairment charges. It is the remaining value of an asset after taking into account any reductions due to depreciation or impairment.  Net carrying amount is an important financial metric as it reflects the asset's current value and is used to determine the overall financial health of a company. By deducting the accumulated depreciation and impairment costs from the asset's initial purchase price, one can determine an investment's net carrying amount. Calculation of Net Carrying AmountCalculating the net carrying amount involves considering the asset's original cost, any accumulated depreciation, and any impairment charges. The formula for calculating the net carrying amount is: Net Carrying Amount = Original Cost - Accumulated Depreciation - Impairment Charges The original cost of the asset is the amount paid to acquire the asset, including any costs recorded to bring the asset to its current state. The amount of the asset's worth that has been depleted over time as a result of damage, obsolescence, or other circumstances is represented by accumulated depreciation. Impairment charges signify a fall in an asset's worth as a result of a long-term decline in value. The Bottom LineAccumulated depreciation is a credit balance because it is a contra-asset account that is used to offset the balance of an asset account. It is important for accurately reporting the value of fixed assets on financial statements and for tax purposes. Companies may make sure that their financial statements are correct and consistent with accounting rules by grasping the idea of accumulated depreciation. |

We provides tutorials and interview questions of all technology like java tutorial, android, java frameworks

G-13, 2nd Floor, Sec-3, Noida, UP, 201301, India